Eastern Europe became a prominent market with solid growth potential for the entertainment industry, and companies are seeking opportunities to build strategic advantages in the region.

Let's figure out why and how the war in Ukraine affects the market.

General overview

Over the past decade, the European gambling market has shown significant growth. Thanks to regulatory bodies collating and reporting jurisdictional online market data, the business has moved out of the shadows and become more transparent. Excluding lotteries, licensed online gambling revenue across Europe is growing year by year: from €17.3 billion in 2019 to €24.6 billion in 2021.

The Covid-19 crisis slowed growth compared to 2019, but accelerated the market transformation from offline to online. In 2021, Europe's online gambling revenue was expected to reach €36.4 billion (41.7% of total gambling) gross gaming revenue (GGR), an increase of 19% compared to 2020. It’s worth noting that among the fastest-growing regulated online markets are countries from Eastern Europe.

At the beginning of 2022, another threat shocked the region—the war in Ukraine. Thousands of lives have been lost, and millions are at stake. Russian aggression has destroyed infrastructure, dealt more than 600 billion in direct losses to Ukraine's economy, changed the global energy landscape, caused irreparable environmental damage, and created the world's largest human displacement crisis. Of course, all these factors and the ongoing crisis have impacted the region's gambling market and player activity.

But let's look at Eastern European markets, which remain promising despite global crises and the hostilities in Ukraine.

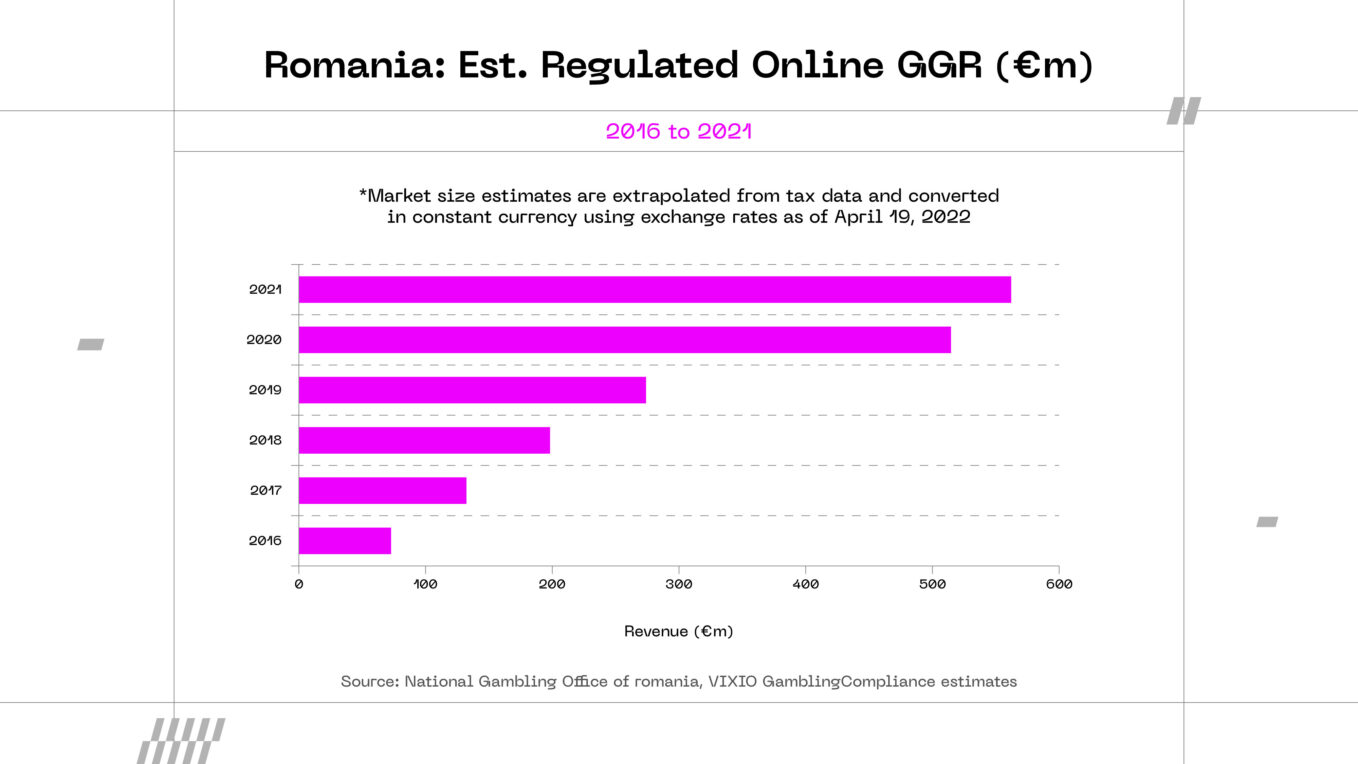

Romania—one of the fastest-growing online markets in Europe

The National Gambling Office (ONJN) regulates the Romanian market, with its wide range of products, via local licences available to private operators.

Alongside secondary legislation and full online gambling licences, GGR is growing yearly. In 2017, Online GGR grew by 84%, in 2018 by 50%, and in 2019 by 39%. The most substantial double-digit growth was in the Covid-19 year when GGR grew by 88%, after which a modest increase of 9% in 2021 failed to match the impressive figures of the preceding years.

The accelerated growth observed in 2020 was the highest of any established regulated online market in Europe and followed by market expansion of 50% in 2018 and 39% in 2019, with full-year GGR having grown more than sevenfold between 2016 and 2020.

The online share of gambling activity in Romania is one of the top 5 indexes across Europe: 56.7% in Romania, 59.3% in the UK, and 59.4% in Denmark. According to the statistics, online betting shares have risen to 60%, almost doubling the 30% share of casino products. Poker, lottery, and bingo combined account for less than 10% of the market.

Licenced online operators in Romania are subject to a 16% tax on incomes collected from gambling activities, but no less than 100 thousand euros per year.

The government set a course for further regulation and development of the gambling industry. For instance, the bill on 40% tax on profits from gambling has been greatly changed, reducing the burden by several times depending on the amount of withdrawal.

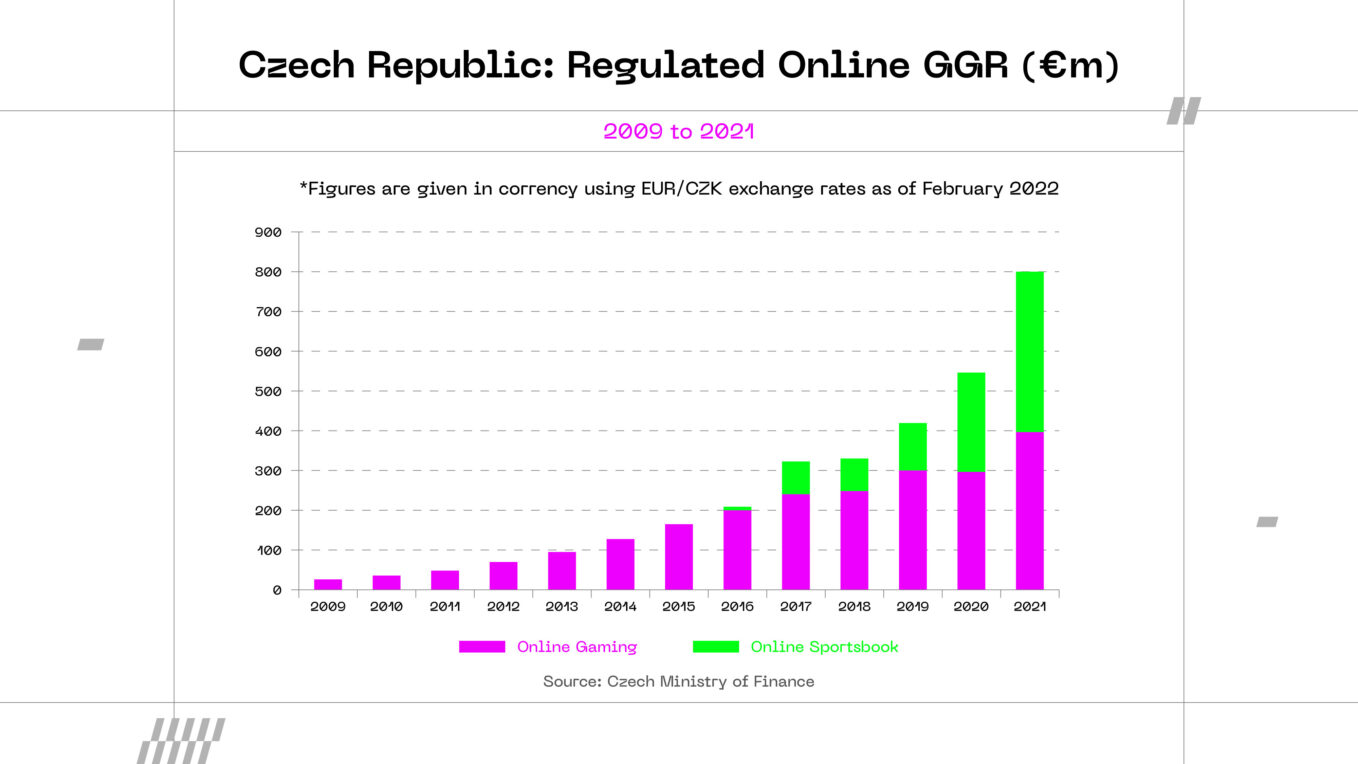

Czech Republic—leading growth potential in Eastern Europe

Since 2017, the Czech Republic has fully regulated online gambling under the oversight of the Ministry of Finance. Current legislation allows all land-based forms of online gambling, including lottery, sports betting, casino games, and card games.

According to the Czech Ministry of Finance, from 2017 to 2021, GGR grew from nearly €330 million to €800 million. The seven years between 2010 and 2017 were characterised by consistent 20% plus yearly growth, moderated to just 3.1% in 2018 before rebounding above the 20% mark in 2019. It’s noteworthy that the central part of the growth in GGR is related to the online gaming share, which is connected to Covid-19 restrictions and the ban on major sporting events.

Online sportsbook revenue in the Czech Republic has grown roughly tenfold over the past decade, spanning both the current and previous licensing regimes, but edged back by 1.7% to CZK7.6bn (€298m) amid the disrupted sporting calendar of 2020.

The statistics show that the republic's online share of the total gambling market revenue ranked 10th among all European countries with growth just below 50%. If we consider the gambling product shares of national gambling markets, in 2020, sports betting was in 1st place with around 48% of GGR, casinos took second place with 40%, 10% went to the lottery, and 2% to poker.

Taxation in the market is set at 23% of GGR for most games, except for lotteries and "technical games" such as online poker, roulette, or gaming machines, which face an internationally high GGR tax of 35%.

The blocklist provided by the Ministry of Finance has significantly prevented unlicensed operators from entering the Czech market. Since 2018, in the name of transparency, the Ministry of Finance has been obliged to obtain court approval before adding new domains to the blocklist.

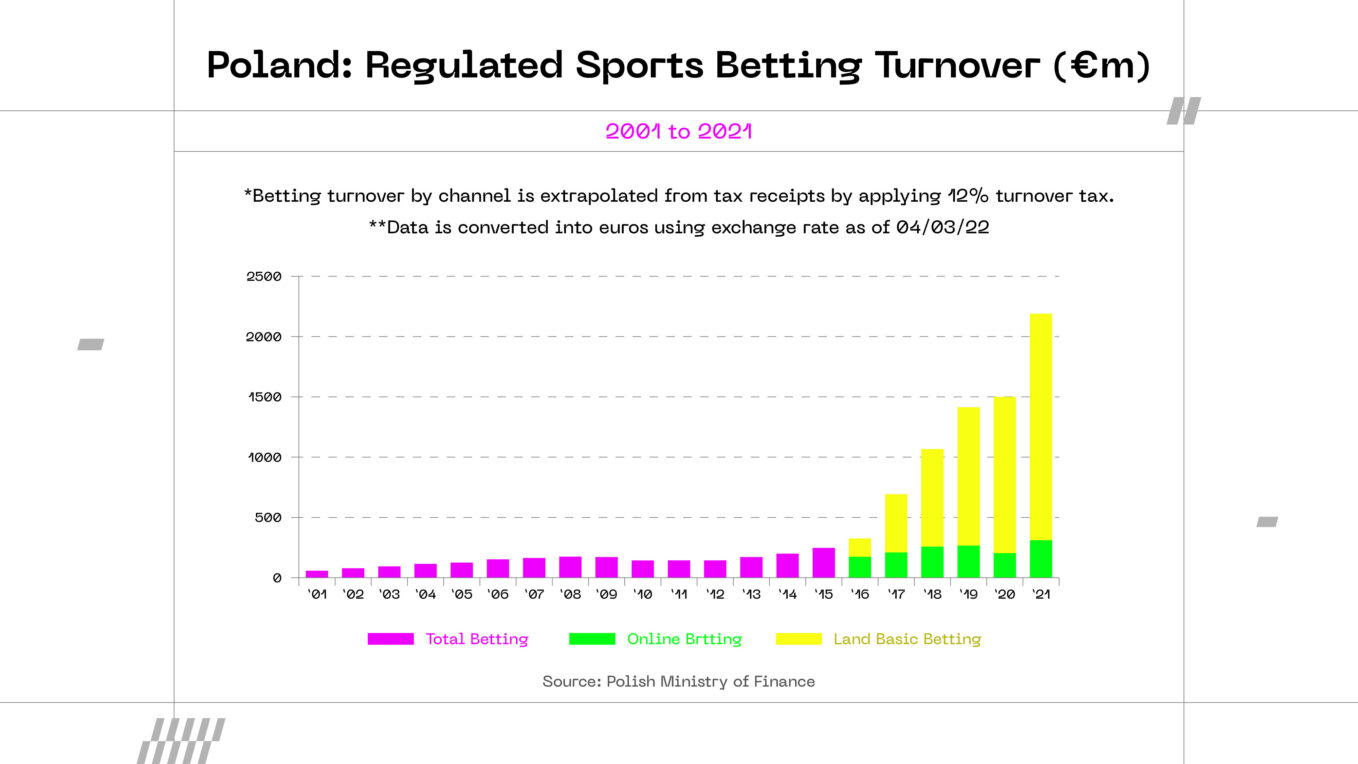

Poland—the strictest regulation in Europe

Poland is a tough market with great potential. Online gambling in Poland is regulated by a state monopoly, except for online betting and promotional lotteries. Betting licences are available to private operators, but these licences don't provide other online products, only betting on sports and horse racing.

According to the Polish Ministry of Finance, in 2021, regulated online GGR exceeded €600 million. The ministry also says that in 2021, betting turnover was over 2 billion euros, which is 46% more than in 2020. The growth dynamics of online betting were positive and stable despite the Covid-19 crisis.

The regulation policies resulted in part of the online betting GGR being way higher than that of online casinos. As for the gambling product shares of the online market, betting was in the lead with more than 50% of GGR. Online casinos were second with more than 23%, and third place went to the lottery with almost 20%. Bingo and poker share 2-3% between them.

Poland's licensed online betting operators are subject to a widely criticised 12% turnover tax left untouched by the 2017 amendments.

The blocklist provided by the Ministry of Finance in May 2022 counted almost 25 thousand domains, showing remarkable work provided to establish regulation in the industry and great interest in the Poland market from operators.

How the war in Ukraine affected the Eastern European gambling market

The military aggression against Ukraine has isolated Russia from the rest of the world, including the gambling market. Indeed, the Russian gambling industry will be damaged by bans on Russia from sports events such as the UEFA Champions League, the cancellation of the Formula-1 Grand Prix, the exclusion of other sports teams and the imposition of sanctions.

Our Parimatch brand was one of the market leaders in Russia and Belorussia, with a solid market share. But the war started by Russia against the Ukrainian people is unacceptable; thus, following all the necessary legal proceedings, we withdrew the Parimatch brand and ceased all operations. DraftKings, FanDuel, Statscore, 888poker and GGPoker, Bet365, PokerStars, and other international market leaders also demonstrated their solidarity with the people of Ukraine and left the Russian market.

The general crisis also affects Eastern European gambling due to changes in the energy market and accelerating inflation. People’s incomes are falling, reducing the amount of money they can devote to entertainment.

But the fall in income doesn't mean people have stopped spending on entertainment. Betting and gambling are primarily about emotions that distract from and relieve stress. In times of worldwide crisis too. Recent studies of the Eastern European market show that the region's interest in betting has been consistently high, with similar activity peaks on weekends and during significant sports events.

The cost of living crisis explains why index peaks are lower than before the 24 of February, but the general level of interest is just the same. Except for Russia, Belorussia and Ukraine, the Eastern European gambling market continues to see sustainable development.